Go to: OVERVIEW

(SaveOurCounty) DETAILS

(listener)

PLANNING SCHOOLS ENVIRONMENT EROSION

Report corrections & broken links to Webmaster Get updates on local issues

Is Your Property Tax Going Up?

Your Property Tax goes up when the Assessed Value goes up. To calculate Property Tax, multiply the Tax Rate (now 1.2% per year in most of the county) times the Assessed Value. The Rate has been pretty stable as shown in the table below, while Values have been going up.

Assessed Value is supposed to be 60% of the Market Value last July 1. If you were 65 or older by last June, or disabled and meet some residence & application requirements, you can get the Homestead exemption: they subtract $20,000 from the Assessed Value.

Market Value is what your property would sell for on the open market, assuming enough time and marketing for a well-informed seller to find a well-informed buyer.

Monongalia County provides some explanations.

You can appeal for a lower value any time before early February. You might ask a real estate appraiser if (s)he can testify & demonstrate that your assessment is too high. If so, or if you can prove it any other way, appeal. One man's odyssey is at http://kensey.googlepages.com/property-tax-appeal-process.pdf

You can get some information from the opposition: the Jefferson County Assessor's office 728-3224. Appraisers are at the office 9-5 Monday-Friday. The office was open until 7pm Fridays in 2005-2008, to let you see maps and ownership records, but very few people came in, so they no longer offer evening hours. Ownership records, maps, taxes & values for previous years are on the web, http://listener.homestead.com in the middle of the page

The Assessor's office can:

(a) Show you a printout describing the traits of your own property: date of construction, number of rooms, AC, judgment of overall building & site quality, etc. Be sure this is accurate.

(b) Show you printouts of recent sales in your subarea of the county. See if these are accurate and comparable. The printouts omit tax sales, sales between relatives, and sales that cover more than one lot, so they leave out what would be the lowest prices on a per lot basis. Subareas should be homogeneous, and may be more or less than a whole subdivision or tax map.

(c) Schedule a hearing in front of the elected County Commissioners by mid-February. They're called the Board of Review and Equalization when they hear tax appeals. They should provide a guide to citizens on how appeals work, and they should have legal advice available, but they don't since the County Prosecutor represents the Assessor in these appeals, not the Commission or the public.

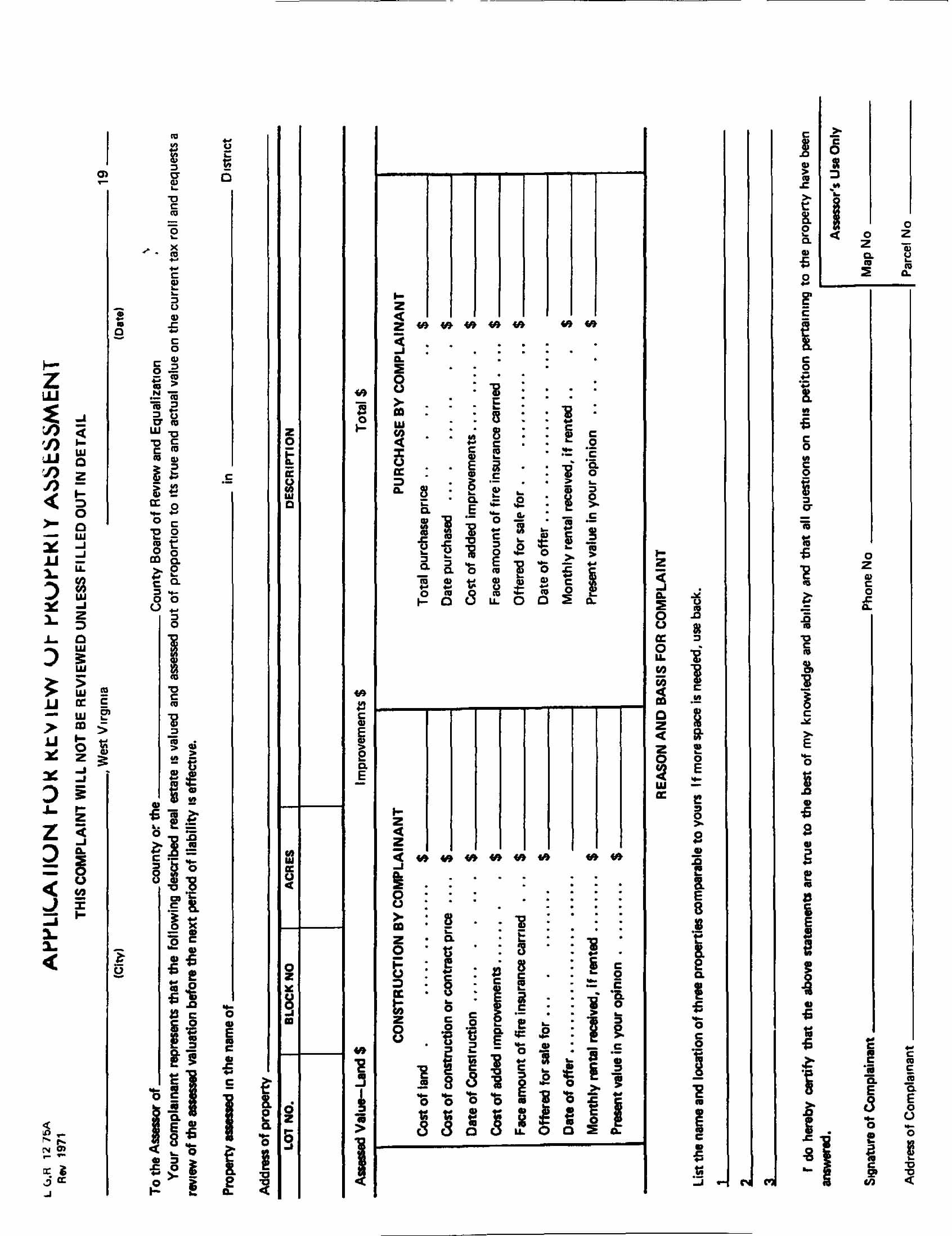

(d) Receive your "complaint form" showing what you paid for the property, what you insure it for, and three properties that you think are comparable. Or you can mail your appeal in care of the Assessor's Office, 104 E Washington St, Charles Town WV 25414 (no email or fax).

More assessment information is at http://listener.homestead.com Click for the appeal form. In all your dealings, be careful about the difference between "assessed value" which is supposed to be 60% of "appraised value" or "market value" (state law 11-1C-7d and 12b). Confusingly, "assess" is a broad term that includes establishing market value, but "assessed value" or "assessment" is the 60% level, not the market level. Even people in the Assessor's office and the Commission can mis-speak sometimes and say one when they mean the other.

The assessor's office also deals with the "sales ratio," which is the ratio of the Assessor's estimate of market value to actual sales price, for properties that sold in a year. When assessors' estimates drop to 90% of actual sales prices, assessments in the subarea need to be raised. The average still doesn't say whether your particular property is high or low compared to the subarea.

The appeal process requires you to identify at least 3 comparable properties. The process is very unfair, though, because the Assessor is not required to identify any specific comparable properties. She uses a computer system (CAMA, Computer-Assisted Mass Appraisal) which averages prices in a subarea of the county and adjusts prices for some, not all, of the traits listed in (a) above. The adjustments were calculated about a decade ago, and may not have been right then. The Assessor claims to show land & improvement values separately, but her land value includes earthwork, well, septic, so it is not comparable to an empty lot.

Last summer you probably received in the mail a blank "Tax Report" to fill out as your own report of the value of property. You were required to submit it by October 1. If you did not submit it on time, some say you are not eligible to appeal.

Burden of Proof: A legal article said in 1995,

there is a presumption of correctness in favor of the assessor's

proposed assessed value, thereby imposing the burden of proof on the property

owner. Nevertheless, even relatively recent judicial authorities seem to be

split as to the standard of proof required to carry that burden and to overcome

the presumption.

Within less than a year's time, the court, in two separate

decisions, stated: (1) that, before the board, an "objecting party ...

must show by a preponderance of the evidence that the assessment is

incorrect" and (2) that, "where a taxpayer protests his assessment

before a board, he bears the burden of demonstrating by clear and convincing

evidence that his assessment is erroneous." (Caryl, "The Illusion of

Due Process," WV Law Review v.98 pp.301-362, Fall 1995)

One case is on the web, from 1993, saying the standard is "preponderance of the evidence" Eastern American Energy v. Thorn

State law 11-3-1 (below) says that even owner-occupied assessments must primarily be based on rental value; The assessor's office ignores this rule.

If Listeners have more information on tax assessments, appeals, or the CAMA program, please write in.

Farms are not taxed on the full market value

of land, but only on the value as farmland, a big break. The assessor finds out

local rent levels each year for each type of farmland: pasture, woodland, and 5

grades of cropland. The annual rent is assumed to be 12% of the value as farmland,

a percentage which is set annually by the state tax office. So taxable value is

rent divided by 0.12. This applies whether farming is done by owner or tenant,

full year or seasonally, For example, if the usual rent for one type of land is

$35 per acre per year the taxable value would be $292 (35/.12) per acre.

Farmland owners apply to the county assessor

in July or August each year. Each tax parcel must be farmed at time of

application and in the previous year, meaning:

1. Parcels with 5 acres or more,

which produce farm products of at least $1,000/year.

2. Parcels less than 5 acres, which produce farm products of at least $500/year

Tax

Rates on Owner-Occupied Homes in Jefferson County

Also called Class 2

Percent of Assessed Value (i.e. dollars per year, per $100 of Assessed Value)

Rentals & Commercial pay twice as much (called Class 3+4)

|

Taxes due in year starting July 1, |

1999 |

2006 |

|

Total,

outside Towns |

1.2184 |

1.2060 |

|

School Excess Levy (chosen by Voters) |

.4360 |

.4590 |

|

School Basic Levy (set by state) |

.4096 |

.4010 |

|

School Bonds (chosen by Voters) |

.0898 |

.1012 |

|

County (set by County Commission) |

.2780 |

.2398 |

|

State (set by state) |

.0050 |

.0050 |

|

Extra in each town: |

|

|

|

Ranson |

.2500 |

.2268 |

|

Charles Town |

.2318 |

.1798 |

|

Shepherdstown |

.1432 |

.1520 |

|

Bolivar |

.1568 |

.1378 |

|

Harpers Ferry |

.1184 |

.1266 |

State law

§11-1C-12b ... each county shall implement a

uniform assessment that is equal to sixty percent of the most current

appraised value for all real and personal property situated within the

county...

§11-3-1. Time and basis of assessments; true and

actual value; default; reassessment; special assessors.

All property shall be assessed annually as

of the first day of July at its true and actual value; that is to say,

at the price for which such property would sell if voluntarily offered for sale

by the owner thereof, upon such terms as such property, the value of which is

sought to be ascertained, is usually sold, and not the price which might be

realized if such property were sold at a forced sale, except that the true and

actual value of all property owned, used and occupied by the owner thereof

exclusively for residential purposes

shall be arrived at by giving primary, but not exclusive, consideration

to the fair and reasonable amount of income which the same might be

expected to earn, under normal conditions in the locality wherein

situated, if rented: Provided, That the true and actual value of all farms used,

occupied and cultivated by their owners or bona fide tenants shall be arrived

at according to the fair and reasonable value of the property for the

purpose for which it is actually used regardless of what the value of

the property would be if used for some other purpose; and that the true and

actual value shall be arrived at by giving consideration to the fair and

reasonable income which the same might be expected to earn under normal

conditions in the locality wherein situated, if rented:

Provided, however, That nothing herein shall alter the method of assessment

of lands or minerals owned by domestic or foreign corporations...

{kind=link}